Have you ever stood at the crossroads of a financial decision, overwhelmed by a sea of offers? Choosing from the myriad of credit cards UK residents are offered can feel like navigating a dense fog without a map. It’s a modern paradox: a tool widely associated with debt can, in the right hands, become a powerful instrument for financial gain. This guide promises to be your compass.

We are here to demystify the world of the best cashback credit cards UK. This isn’t about promoting reckless spending or chasing magical returns. Instead, we will treat this as a psychological tool for financial empowerment—a practical framework for turning your necessary expenses into a tangible asset. Let’s peel back the layers of jargon and discover not just a card, but a strategy.

Article Contents

- Understanding the Essence of Cashback

- The Archetypes of Cashback Cards

- Journeys in Cashback: Real-World Scenarios

- Actionable Solutions: Your Path to Maximising Rewards

- Relevance in the Modern World: Cashback in the Cost-of-Living Crisis

- Conclusion: The Enduring Wisdom of Financial Empowerment

- Your Next Step

- Context and References

Understanding the Essence of Cashback: A Principle of Value Exchange

At its core, a cashback credit card is a financial product that refunds you a percentage of the amount you spend on it. This is not ‘free money’, but rather a calculated rebate. Its origin lies in the simple economic principle of incentives. Each time you use your card, the merchant pays a transaction fee (the ‘interchange fee’) to the card issuer’s bank. The bank, in turn, shares a small portion of this fee back with you as a ‘thank you’ for using their card.

Understanding this mechanism is crucial. It transforms the concept from magic into a logical system of value exchange. You provide transaction volume to the bank; the bank provides you with convenience and a small financial return. This is knowledge, not a prophecy of wealth. It’s a guide to making your existing spending work smarter for you.

The Archetypes of Cashback Cards: Finding Your Financial Match

Not all cashback cards are created equal. They possess different ‘personalities’ or archetypes, each suited to a different lifestyle and spending pattern. Identifying your own pattern is the key to choosing wisely.

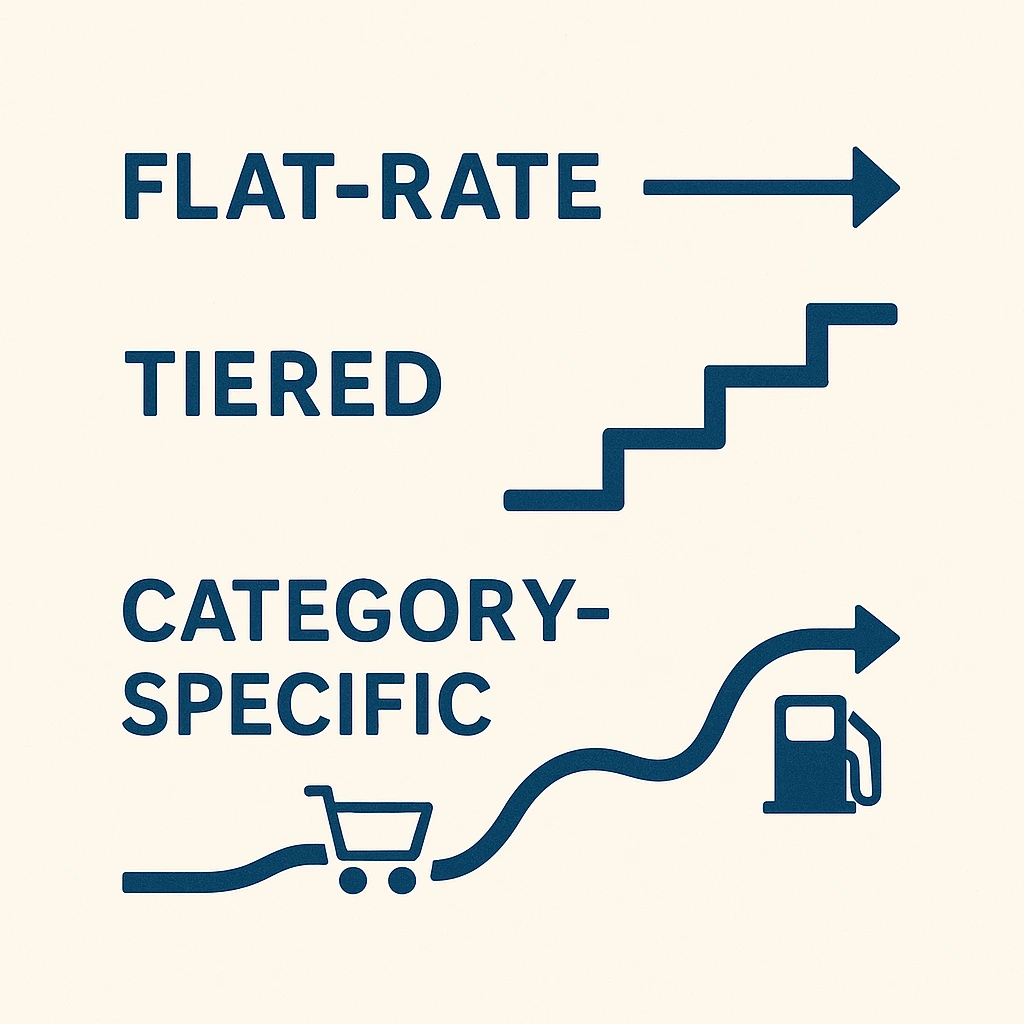

The Consistent Generalist: Flat-Rate Cards

This card archetype is the dependable workhorse. It offers a single, flat percentage of cashback on every purchase, regardless of the category. Its strength lies in its simplicity and predictability. There are no categories to track or spending tiers to meet. The paradox? While reliable, its cashback rate is often lower than the potential maximums of more complex cards. It’s perfect for those who value simplicity over micromanagement.

The Ambitious Climber: Tiered Cards

This card rewards higher spending. It may offer a low introductory rate (e.g., 0.25%) on the first £5,000 spent annually, which then ‘climbs’ to a much higher rate (e.g., 1% or more) thereafter. Its positive side is the high potential reward for big spenders. The inherent contradiction is that it can be punitive for those who don’t spend enough to reach the higher tiers, leaving them with a subpar return. This archetype suits households with significant, consistent annual expenditure.

The Focused Specialist: Category-Specific Cards

This is the expert. It offers significantly higher cashback rates (sometimes 3-5%) in specific categories, like groceries, fuel, or dining, while offering a standard low rate on everything else. Its power is its ability to supercharge rewards in your highest spending areas. The duality is clear: its value plummets if your spending doesn’t align with its specialities. It’s ideal for the strategic consumer who doesn’t mind using different cards for different purposes.

Journeys in Cashback: Real-World Scenarios

Theory is one thing; application is another. Let’s see how these archetypes play out in real life.

Scenario 1: The Young Family and the Weekly Shop

Meet the Harris family. Their largest monthly outgoings are groceries and fuel for the school run. They were using a simple flat-rate card, earning a modest £5-£7 per month. The conflict was a feeling that their biggest expenses weren’t being rewarded effectively. After an audit, they realised the power of a ‘Focused Specialist’ card that offered 3% back on supermarket and petrol spending. The ‘Aha!’ moment came three months later when they saw their cashback had tripled to over £20 per month—simply by aligning their card to their life. This “ancient wisdom” of aligning tools with purpose brought them a tangible, modern benefit.

Scenario 2: The Busy Professional and Simplicity

Amelia is a consultant who travels frequently. Her expenses are varied—flights, hotels, client dinners, software subscriptions. She tried a complex system of category-specific cards but found the mental load of tracking them stressful. The paradox was that in chasing maximum rewards, she was losing peace of mind. Her realisation was that her time was more valuable than the extra 0.5% she might gain. She switched to a premium ‘Consistent Generalist’ flat-rate card. The solution wasn’t just financial; it was psychological. The card gave her a solid, predictable return on all her spending with zero effort, freeing her mental energy for her work.

Actionable Solutions: Your Path to Maximising Rewards

Understanding is the first step, but true transformation comes from practice. Here are concrete steps to apply this knowledge.

Practice 1: The Mindful Spending Audit

Before you look at any cards, look at yourself. For one month, track every penny you spend. Use a simple app or a notebook. At the end of the month, categorise your spending. This is not a ritual of judgment, but an empowering act of self-awareness. It reveals the truth of your financial habits and tells you which card archetype will serve you best.

Practice 2: Compare the Core, Not Just the Crown

When comparing cards, look beyond the headline cashback rate. Consider these factors:

- Annual Fee: Does the cashback earned easily outweigh the fee? For most people, a no-fee card is the best start.

- APR (Interest Rate): If you ever carry a balance, a high APR will wipe out any cashback gains instantly. The golden rule is to pay your balance in full every month.

- Caps and Limits: Is there a cap on how much cashback you can earn per month or year?

This practice is about seeing the whole system, not just the alluring promise.

Timeless Strategy for Modern Times: Cashback in the Cost-of-Living Crisis

In an era of rising inflation and a persistent cost-of-living crisis, every pound matters. The ancient wisdom of making your resources work for you is more relevant than ever. A cashback strategy is not about extravagance; it’s a defensive financial manoeuvre. It provides a small but consistent rebate on non-negotiable expenses like food, fuel, and utilities. In a digital, increasingly cashless society, where every transaction is electronic, leveraging this flow of money is a modern survival skill. It’s a tangible benefit that puts money back into your pocket to offset rising prices.

Conclusion: The Enduring Wisdom of Financial Empowerment

We began by seeing the world of credit cards UK as a confusing maze. By demystifying the process and understanding the archetypes, we’ve transformed it into a set of tools. The ultimate goal is not to accumulate points, but to achieve a sense of control and empowerment over your financial life. Choosing the right card is an act of self-knowledge and strategy, a small but meaningful step on the path to financial well-being.

“The wisest financial strategy is not about earning the most, but about understanding the most. From understanding comes control, and from control comes peace.”

Context and References

Internal Links to Related Articles

- Read more about the universal principles of budgeting here.

- Understanding APR and Credit Card Debt: A Deep Dive.

- Travel Rewards vs. Cashback: Which is Right for You?

External References (E-E-A-T)

For impartial comparisons and consumer advice, we recommend these authoritative sources:

Disclaimer: This content is provided for educational and informational purposes only. The concepts discussed offer guidance for self-reflection and personal financial strategy, not deterministic financial advice. Always conduct your own thorough research and consider consulting with a qualified financial advisor before making any financial decisions.